CoreVest mortgages to New Haven landlords.

First of two parts.

(Updated) A giant California-based commercial lender pumped over $117 million into New Haven this year to help poverty-focused investor-landlords amass more property — raising concerns in the process about the monopolization of local low-income housing, driving up of sale prices for aspiring homeowners, and, potentially, a replay of the 2008 Great Recession.

CoreVest image / Thomas Breen photo

That lender is called CoreVest American Finance.

The Irvine, California-based company specializes in lending to investor-landlords who buy, renovate and rent out one-to-four-family homes.

CoreVest then packages those landlord loans into mortgage-backed securities, which investors from across the world can buy into and profit from if the borrowers of the underlying loans stay current on their mortgage payments.

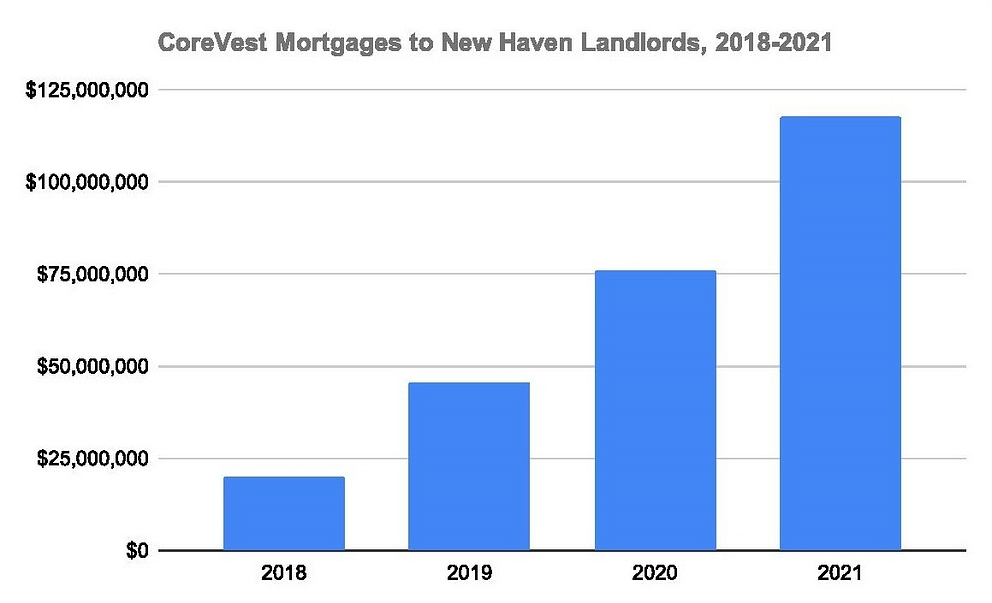

According to the city land record database, CoreVest has dramatically increased its financing of New Haven landlords this year.

In 2021 so far, the company has issued 20 different mortgage loans to local landlords. Those loans total more than $117 million and are secured by hundreds of New Haven rental properties.

That marks a jump from the $75 million CoreVest lent to New Haven landlords in 2020, which in turn was up from $45 million lent to city landlords in 2019, which in turn was up from nearly $20 million lent to city landlords in 2018.

The two biggest winners of CoreVest’s 2021 investments in New Haven’s housing market, meanwhile, are affiliates of the city’s two fastest growing megalandlords: Mandy Management and Ocean Management.

Companies affiliated with Mandy Management’s Menachem Gurevitch received nine different CoreVest loans totaling more than $89.3 million this year.

Companies affiliated with Ocean Management’s Shmuel Aizenberg pulled in eight different CoreVest loans totaling more than $20.1 million this year.

With all that cash and credit flowing their way, Mandy Management in particular went on its biggest buying spree yet.

According to the city land records database, Mandy affiliates spent over $58 million this year buying 179 properties containing 558 different apartments, mostly in low-income neighborhoods far from the city center.

That was up from the $37 million Mandy affiliates spent buying 390 apartments citywide in 2020, which in turn was up from the $16 million they spent buying 186 apartments in New Haven in 2019, which in turn was up from the $13 million they spent buying 173 apartments in New Haven in 2018.

Recent credit rating agency reports about CoreVest mortgage-backed securities, meanwhile, make clear that the money flowing to New Haven from this California-based commercial lender directly helped local investor-landlords expand and expand and expand.

“Loan proceeds were used to refinance existing debt and pay closing costs,” one report states about a $26.6 million loan CoreVest lent to a Mandy affiliate in September.

“The loan proceeds were used to acquire a portion of the underlying homes and refinance existing debt encumbering the other portion of the collateral properties,” reads another report about a separate $25.6 million loan CoreVest lent to a Mandy affiliate in March.

“The mortgages pulled are existing loans that were refi’d because they were close to maturity. The excess funds will be used to acquire additional properties in New Haven,” an Ocean representative told the Independent in August when asked about over $3 million in recent CoreVest-to-Ocean mortgage loans.

All of this comes at a time when global investors and Wall Street-backed firms are seeking to cash in on the Great Recession-rebound by plowing billions of dollars into buying up “distressed,” foreclosed and formerly owner-occupied housing all across the country, and turning those homes into rentals.

It also comes as the city has taken Gurevitch and Aizenberg to state housing court over persistently unfixed code violations at some of their local rental properties. (Click here and here for stories on each of those landlord’s responses to those court cases, including critiques of the city for poorly communicating with landlords about what needs to be fixed, when. Those landlords also argue that they don’t just buy properties; they also spend millions of dollars fixing them up to make them better places to live. Click here for an article from the end of last year with different takes on Mandy as a landlord.)

What exactly is Corevest?

How does their business model work?

And what do CoreVest’s stepped-up investments in megalandlords like Mandy and Ocean — as well as their financing of housing in the form of mortgage-backed securities — portend for the future of living in New Haven?

The lenders and landlords are not accused of breaking laws through these legal transactions. Rather the concern is, as longtime local affordable-housing innovator Jim Paley characterized it, a driving up of low-income housing costs and “the deepening of a divide between affluent neighborhoods and low-to-moderate-income neighborhoods” through practices that mirror the lead-up to the 2008 market collapse.

CoreVest, Explained

CoreVest President Christopher Hoeffel.

Previously known as Colony American Finance, CoreVest was formed in 2014 by the private equity real estate firm Colony Capital, Inc.

In 2017, it was acquired by the global real estate investment company Fortress Investment Group.

And in 2019, its operating platform and $900 million of “related financial assets” changed hands yet again — this time falling under the ownership of the real estate investment trust, Redwood Trust Inc.

In a phone interview with the Independent, CoreVest President Christopher Hoeffel described his company’s business model as benefiting landlords, renters, and international investors alike.

“We provide capital to landlords,” he said. “They are using that capital to buy properties, to fix them up, to create more housing units.”

Unlike most real estate mortgage lenders, Hoeffel said, CoreVest finances only investors — not homeowners.

It specializes in lending to small and mid-sized investor-landlords who own single-family rental (SFR) properties. (In the landlord financing world, “SFR” refers to one-to-four-family rental units.)

“There were no reliable sources of debt financing for investors in housing” before CoreVest was founded in 2014, he said. Those investor-landlords could go to the GSEs [Government-Sponsored Entities] like Fannie Mae and Freddie Mac on a limited basis, he said. Or they could get personal loans. That made the cost of borrowing quite high for investors buying up rental housing. He said that the cost of borrowing for landlords has come down over the years since CoreVest came into being “because we’re providing reasonably priced financing to landlords.”

How does this benefit tenants living in the one-to-four-family rental housing at the center of CoreVest’s business?

Hoeffel said that many of the properties his company finances are old or on the brink of falling out of the housing market altogether.

He said CoreVest’s loans to landlords often help pay for a new bathroom, a new kitchen, and a better place to live.

“We’re actually creating more housing, viable housing, out of what was otherwise obsolete,” Hoeffel said.

As for the landlords, “We’re providing them very reasonably priced financing to the property. They have the liquidity they need to renovate, improve the property, and put it out into the housing market.” And, of course, to grow their holdings.

And for the investors who put their money into the mortgage-backed securities that are made up of these underlying landlord loans?

“It gives them exposure to U.S. housing,” Hoeffel said. He said CoreVest’s landlord-loan securities allow institutional investors like insurance companies and money managers and even sovereign wealth funds to profit off of this country’s housing market.

“We will aggregate a portfolio of loans that will create a steady cash flow stream over five to 10 years,” Hoeffel said, “then issue bonds backed by the portfolio of mortgages.”

He said CoreVest’s average portfolio loan has a loan-to-value ratio (LTV) of 67 percent. That’s relatively low, he said, meaning that investors can make money off of the U.S. housing market while not exposing themselves to too much risk in the form of a borrower who can’t keep up with their loan payments.

The article describes how CoreVest’s then-parent company, Colony Capital, was one of three big private equity firms to seize the Great Recession-recovery moment by “betting that so-called landlord loans to small and midsize investors will become the next big opportunity to profit from the rebound in the United States housing market.”

They did so by providing billions of dollars’ worth of loans to real estate funds that gobbled up “distressed” homes and turned those properties into single-family and multi-family rentals. Those same firms then bundled those landlord loans into bonds, or mortgage-backed securities, and sold those securities piece by piece to investors.

According to recent credit rating agency reports on some of CoreVest’s mortgage-backed securities, CoreVest has been quite successful at lending to landlords and securitizing those loans since first getting into the business seven years ago.

One report states that CoreVest American Finance — or CAF — has a “team of 125 employees in four offices in addition to one regional originator. The senior management team has an average of more than 20 years of relevant experience. As of September 30, 2021, CAF entities had originated approximately $11.7 billion of SFR loans made to over 5,000 borrowers across 48 states and Washington, D.C.”

Another rating agency report reads: “Although the company and, therefore, the team have only been in place for a relatively short period, this is mitigated by the strong securitization, origination and underwriting experience of the managers, originators and underwriters. CoreVest sources loans directly and through third parties and loan purchases. This sourcing includes internal origination teams, marketing initiatives, external broker networks, wholesale partners, relationships with external originators and portfolio purchases.

“The company has groups that focus on the origination, underwriting and closing of loans. Relationship managers and analysts source loans via direct outreach to brokers, borrowers and property managers and conduct the underwriting, screening and loansizing for prospective loans.”

That same report states that, before CoreVest’s acquisition by Redwood Trust in 2019, the company was “the largest and most active lender within the single-family rental space in which it operates.”

Why New Haven

Kroll Bond Rating Agency

Some New Haven rental properties covered by landlord loans included in CoreVest American Finance 2021-3 Trust.

Given CoreVest’s size and stature and deep pockets in the world of landlord financing, why direct so much of its money towards the relatively small housing market of New Haven?

And why towards landlords like Mandy and Ocean in particular?

Hoeffel said that CoreVest started lending to New Haven investor-landlords back in 2014. So it has been involved in the New Haven housing market since the company first came into being.

“We like New Haven because it’s got a very large rental housing stock,” he said.

“The investors that we finance are focused on buying infill housing and renovating it and making what might otherwise be obsolete housing, viable rental housing.”

He commended both Mandy’s Menachem Gurevitch and Ocean’s Shmuel Aizenberg for their companies’ track records as CoreVest borrowers.

“We’ve had a long-term relationship with them,” he said. “We’ve been helping them to grow their portfolios.”

Why such a significant increase in funding of New Haven investor-landlords this year in comparison to previous years?

“It’s because our borrowers have been growing,” Hoeffel said. “It’s not that we’re targeting New Haven more than any other markets.”

In comparison to other cities that CoreVest lends in, like Chicago and Atlanta and Detroit, New Haven’s population and housing stock are relatively small. And as rating agency reports show, New Haven plays a disproportionately large role in CoreVest’s landlord lending portfolio.

Kroll Bond Rating Agency data

Geographic distribution of landlord loans included in CoreVest American Finance 2021-3 Trust.

For example, the mortgage-backed security CoreVest American Finance 2021 – 3 Trust consists of 70 landlord loans totaling nearly $303.7 million, and covering 3,398 apartment units in 22 states.

Over 14.5 percent of those mortgaged apartments, or 493 units in total, are located in the New Haven-Milford Metropolitan Statistical Area (MSA). And roughly 14.3 percent of the trust’s underlying loans, or $43.3 million, went to New Haven landlords.

That means that loans on New Haven rental properties make up the greatest percentage of any geographic area represented in the trust — coming in higher than CoreVest loans issued to landlords in the much larger cities of Chicago, Atlanta, and Houston.

So, again, why New Haven?

“We like these Northeast markets,” Hoeffel repeated. “They have a stable housing stock, not a lot of new construction, and a lot of investors buying older housing and renovating them and making them into viable rental housing.”

Mandy: "Strong Working Relationship"

Mandy’s Yudi Gurevitch was asked for comment on the role that CoreVest plays in Mandy Management’s overall business plans and on the local megalandlord’s stepped-up expansion in New Haven’s rental housing market.

“CoreVest is a leading independent lender to real estate investors nationwide,” he replied.

“For several years, we have established a strong working relationship with CoreVest and enjoyed a solid, productive customer-vendor relationship. We do not have a strategic partnership with the firm. We operate independently and focus on creating long-term value for our investors, customers, suppliers and employees.”

An October pre-sales report by Fitch Ratings about the mortgage-backed security CoreVest American Finance 2021 – 3 Trust also makes clear that CoreVest is not the only — or even the primary — source of financing for Mandy’s investor-landlord affiliates.

“The sponsor has been active in CRE [commercial real estate] for over 25 years and currently operates a portfolio of $385.0 million throughout New York City, Miami, Fort Lauderdale, Bridgeport, CT and New Haven, CT,” that report reads about Mandy Management’s affiliates.

“The company was initially founded in Brooklyn, NY, where the sponsor acquired its first property before eventually entering the New Haven, CT market, which is where a majority of the portfolio is currently centered. The sponsor owns approximately 2,500 SFR properties throughout the New Haven, CT MSA. The sponsor initially sourced financing from personal relationships with local investors but has since partnered with larger Israeli investors, which is where the majority of the current funding originates from.”

Paley: Bubble Burst Redux?

Paul Bass file photo

Neighborhood Housing Services of New Haven Executive Director Jim Paley.

CoreVest’s increasing investments in New Haven megalandlords concern Neighborhood Housing Services of New Haven Executive Director Jim Paley.

Since the 1980s, Paley and his local nonprofit have bought derelict properties in lower-income neighborhoods like Newhallville, gut-rehabbed homes, and sold them at affordable prices to first-time homeowners.

Paley said that CoreVest’s enabling of investor-landlords like Mandy and Ocean to grow and grow by pouring tens of millions of dollars into this market every year has several significant impacts on New Haven housing.

For one, it makes it a lot more expensive for others to buy.

“It’s driving up prices,” he said. “It’s making housing less affordable.”

Because these investor-landlords have so much cash and credit on hand, and because New Haven’s housing market — like the country’s — is already experiencing a bit of a pandemic-induced heat-up — “the houses that are on the private market are going for over asking price,” Paley noted.

“Nobody is going to be doing the gut renovations that we would do on these properties. They’re going to remain substandard housing, rental housing” unless — and this is a big “unless,” he said — the city significantly steps up its enforcement of the residential licensing and housing code enforcement program.

That’s the second big risk and impact, Paley said: That residential buildings that could provide opportunities for homeownership are instead sucked into the rental market for the long term.

“Instead of bringing our neighborhoods together as a city, [these types of investments] are actually fomenting a divide between the affluent neighborhoods and the low-to-moderate-income neighborhoods,” Paley said.

“What this is doing is it’s giving those investors an opportunity to expand even further,” he continued. “It is wedging a divide between the market-rate housing and downtown development, and the neighborhoods that they are acquiring additional properties in.”

Which brought Paley to his third, big-picture concern.

CoreVest’s lending to landlords and packaging loans into mortgage-backed securities “is very reminiscent of the pre-2008 housing bubble bursting,” he said.

He noted how banks bundled risky mortgages into deceptively toxic investment instruments that ultimately helped push the worldwide economy into freefall.

CoreVest’s mortgage-backed securities seem geographically diversified enough that “if one mortgage market declines and defaults, that would be covered by other strong landlords,” Paley said, likely avoiding the type of mass economic hurt that could be felt if some of their landlord-borrowers suddenly couldn’t pay their loans back.

Kroll Bond Rating Agency (KRBA) points toward this very concern in an October pre-sale report in which it evaluates the strengths and weaknesses of the mortgage-backed security CoreVest American Finance 2021 – 3 Trust in general, and of an underlying $26.6 million loan recently issued to a Mandy affiliate in particular.

All 121 properties covered by that loan “are located in the New Haven-Milford, CT CBSA,” the report notes. “A geographically concentrated pool of properties can be significantly more exposed to defaults and losses due to a downturn in the local economy and/or property markets relative to a more diversified portfolio.”

BRRRR: Buy, Rehab, Rent, Refinance, Repeat

Thomas Breen file photo

Jacob Miller.

Jacob Miller — a former Mandy employee who now co-runs a local real estate brokerage and software development firm — told the Independent that this type of conversion of low-income housing into financial instruments is an all-too-common practice among savvy, successful real estate investment firms that know how to grow.

“This is honestly very standard and part of the overall strategy for many of the more sophisticated (large & small scale) landlords,” Miller stated by email. “It can work when you are using a hard money loan or non-QM investor mortgage, but works even better when employing a cash acquisition strategy.”

Here’s how it often works, he said: Landlords acquire properties via cash purchases. They then renovate and rent them out to create “positive cash flowing assets.”

As market values rise, landlords then turn to commercial lenders like CoreVest and take out a mortgage on the whole “cashflow positive portfolio (generally with a 75% Loan to Value ratio).”

This strategy even has a name, he said: BRRRR, for “Buy, Rehab, Rent, Refinance, Repeat.”

Miller, a New Haven native, previously worked for a Milford-based mortgage lender as well as for Mandy. The experience has led him to become an outspoken critic of what he described as Mandy’s “disaster capitalist” business model of directing rent and outside investment into new acquisitions rather than into maintenance and capital repairs. (Mandy’s Yudi Gurevitch has defended his company as spending millions every year on maintenance and repairs. See here and here for Gurevitch’s responses to that insufficient-upkeep critique.)

When asked for comment on Mandy’s recent loans from CoreVest and CoreVest’s subsequent packaging of those loans into mortgage-backed securities, Miller stressed that this is how the real estate investment world has come to work.

Securitization of landlord loans is “par for the course,” he wrote.

“While I personally have issues with this practice, it’s a massive industry and mortgage backed securities are historically considered low risk and diversified.,” he said. “This type of portfolio is also traditionally very profitable due to the high prevalence of tenants using section 8 vouchers and other subsidized programs.”

So long as there is an affordable housing crunch and a years-long waiting list for federal rental subsidies, he said, megalandlords who own low-income housing effectively “own an endless supply of tenants without many other housing options.”

Those low-income renters in need of places to live, and backed by federal subsidies, help keep Mandy’s apartments full.

Mandy’s high occupancy and rent collection rates in turn result in a more attractive real estate portfolio for lenders looking to loan, and for investors looking to park their money in a mortgage-backed trust like CoreVest’s.

Indeed, the Fitch pre-sales report on CoreVest American Finance 2021 – 3 Trust states that “approximately 35% to 45% of tenants throughout the portfolio” — that is, throughout the hundreds of New Haven apartments covered by the CoreVest-to-Mandy loans included in this trust — “receive Section 8 subsidies or some other rental subsidy.”

Miller said that the list of local recipients of CoreVest loans skews so much in the direction of investor landlords like Mandy and Ocean for a simple reason: CoreVest doesn’t originate conventional mortgages, so they would never be used by an average homebuyer.

“They are only writing loans for investors with portfolios of cash flowing investment properties.”

He also noted that CoreVest has a good reputation locally for being able to get these types of portfolio loans done — with a focus on portfolios of single and two-to-three family properties, “which some of the larger portfolio lenders won’t underwrite or offer less attractive terms on.”

CoreVest, and its parent company Redwood Trust, is just one of many companies/banks that do commercial portfolio originations, he said. As far as he’s aware, they don’t have any sort of negative reputation.

What are the potential consequences, if any, of New Haven housing stock turning into financial instruments geared towards international investment?

“The main risk is that as an entity like Mandy grows,” Miller said, “they get to do this on a larger and larger scale, cementing their position in the market and monopolizing low income housing as we have seen in New Haven.”

Who Got How Much From CoreVest

Below is a full list of mortgage loans provided by CoreVest to local landlords in 2021, followed by a full list of local CoreVest mortgages from 2020. The names in parentheses are the individuals or companies that control the limited liability companies (LLC) that received the mortgage loans.

And click on the map above to see all of the local properties covered by CoreVest mortgage loans issued to New Haven landlords in 2021.

2021 CoreVest Mortgages to New Haven landlords

SFR 2 DE LLC (Mandy Management): $26,590,000

Ref II SFR 1 DE LLC (Mandy Management): $25,600,000

Netz Bonds New Haven V Add DE LLC (Mandy Management): $11,073,000

Sap Re Holdings LLC (Ocean Management): $10,000,000

Netz Keren De LLC (Mandy Management): $9,646,000

Hemingway Capital LLC (Daniel Scherban, Joseph Scherban): $5,000,000

ABCD Properties DE LLC (Mandy Management): $4,998,000

Real Estate Group XV DE LLC (Mandy Management): $3,000,000

Gantz LLC (Mandy Management): $2,963,000

ABCD Chapel DE LLC (Mandy Management): $2,870,000

Danny and Guy 1 Owner LLC (Mandy Management): $2,625,000

James P DE2 LLC (Barnett Brodie): $2,400,000

VR Investments Delaware LLC (Ocean Management): $1,931,000

280 Winthrop Del LLC (Ocean Management): $1,667,400

Aqua Home DEL LLC (Ocean Management): $1,593,500

Pointer DEL LLC (Ocean Management): $1,541,000

Ocean 90 Delaware LLC (Ocean Management): $1,464,000

Linato Delaware LLC (Ocean Management): $1,166,000

YG RE DEL LLC (Ocean Management): $836,500

CBNH Del LLC (Menachem Ezagui): $677,000

2020 CoreVest Mortgages to New Haven landlords

Sap Re Holdings LLC (Ocean Management): $10,000,000

Ocean 60 LLC (Ocean Management): $7,883,000

GNH II DE LLC (Mandy Management): $5,133,000

Hemingway Investment Holdings LLC (Daniel Scherban, Joseph Scherban): $5,000,000

Real Estate Group XII DE LLC (Mandy Management): $4,358,000

CLLYTREPORPNEVAHWEN, LLC (Jianchao Xu): $4,076,000

BBYM DE2 LLC (Barnett Brodie): $3,800,000

Riley Group DE2 LLC (Barnett Brodie): $3,175,000

Ocean 70 Del LLC (Ocean Management): $3,143,200

Real Estate Group XIV DE LLC (Mandy Management): $2,786,000

Ocean IV Del LLC (Ocean Management): $2,688,000

RBC DE2 LLC (Barnett Brodie): $2,658,500

Real Estate Netz Group DE LLC (Mandy Management): $2,610,000

Sperry Group DE2 LLC (Barnett Brodie): $2,562,300

Alden Elm Del LLC (Ocean Management): $2,505,000

Woolsey Holdings Del LLC (Ocean Management): $2,371,500

Ocean 30 Delaware LLC (Ocean Management): $1,665,000

Real Estate Group XIII DE LLC (Mandy Management): $1,569,000

Ocean 103 Del LLC (Ocean Management): $1,488,000

Ocean 101 Del LLC (Ocean Management): $1,438,000

CMS Realty 2 LLC (Shneor Edelkopf): $1,293,000

Enter Alba Del LLC (Ocean Management): $1,278,700

Ocean 7 Del LLC (Ocean Management): $1,153,000

L&B Venture Properties LLC (Shmuel Levitin): $1,029,000

Shelton Ventures LLC (Jacob Schattner, Jonathan Schattner): $178,500

Given that we cannot control the global market for Mortgage Backed Securities, the real issue here is that local landlords are refinancing properties not to improve them, but to purchase more properties, cornering the market and continuing to let properties decay. The answer to this should be highly aggressive enforcement of building codes and blight ordinances.

To put this is scale, if you add up NHVs grand list for Res/Comm/Ind you get about $8B. So this $100M represents about 1.5% of that. Seems small but on the other hand, everyone knows what one neglected house can do to a good block. NHV officials should not tolerate decay.